Wood countertops are a popular choice for homeowners looking to add warmth and natural beauty to their kitchen or bathroom. However, the cost of installing wood countertops can be a significant investment. Fortunately, there are financing options available, such as personal loans, that can make it easier for homeowners to afford this upgrade. In this article, we will explore the advantages of financing wood countertops using personal loans, highlighting the benefits and considerations that homeowners should keep in mind.

One of the primary advantages of using a personal loan to finance wood countertops is the flexibility it offers. Unlike other financing options, personal loans provide borrowers with the freedom to use the funds as they see fit. This means that homeowners can use the loan to cover the cost of materials, installation, or any other related expenses. Additionally, personal loans typically have fixed interest rates and predictable monthly payments, making it easier for homeowners to budget and plan for the expense.

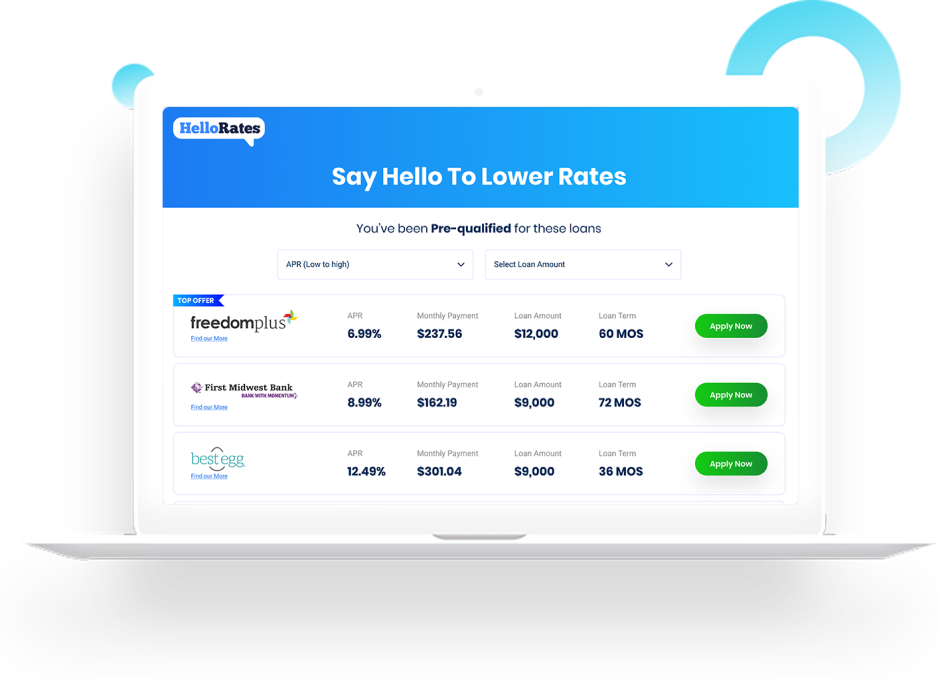

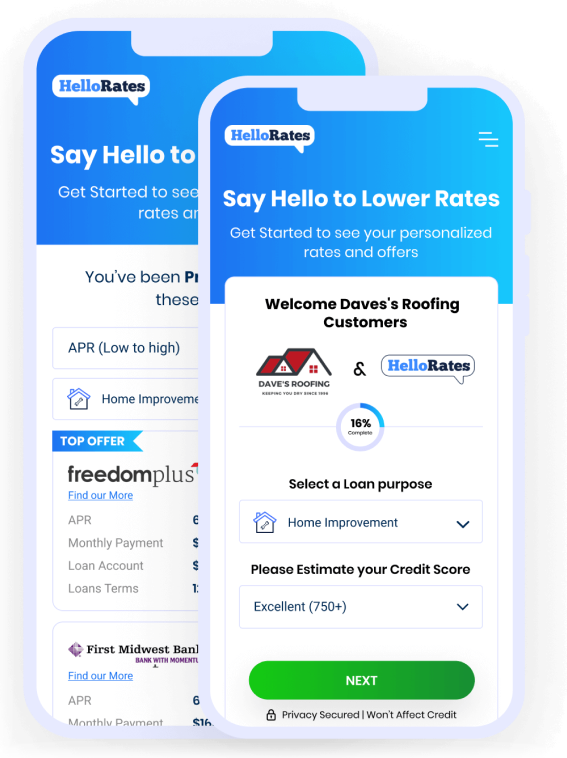

Another advantage of financing wood countertops with a personal loan is the speed and convenience of the application process. Many lenders offer online applications, allowing homeowners to apply from the comfort of their own homes. The approval process for personal loans is often quicker compared to other types of loans, with some lenders providing same-day approval. This means that homeowners can access the funds they need promptly, enabling them to start their wood countertop project without delay.

Personal loans also offer homeowners the advantage of potentially lower interest rates compared to other financing options. The interest rates on personal loans are typically based on the borrower’s creditworthiness, with those who have good credit scores being eligible for more favorable rates. By securing a lower interest rate, homeowners can save money over the life of the loan, making wood countertop financing more affordable in the long run.

Furthermore, financing wood countertops with a personal loan allows homeowners to maintain their financial flexibility. Unlike other financing options, personal loans do not require collateral, such as a home equity line of credit. This means that homeowners can keep their assets separate and avoid the risk of losing their home or other valuable possessions in the event of default. Personal loans also do not restrict the use of credit lines, allowing homeowners to pursue other projects or investments simultaneously.

It is important to note that while personal loans offer numerous advantages, homeowners should carefully consider a few factors before opting for this financing option. Firstly, borrowers should assess their ability to repay the loan within the agreed-upon terms. Personal loans typically have fixed repayment periods, and missing payments or defaulting on the loan can negatively impact the borrower’s credit score. Therefore, homeowners should ensure that they have a stable income and a realistic repayment plan in place before taking on a personal loan for wood countertop financing.

Additionally, homeowners should compare loan offers from different lenders to find the most favorable terms. Interest rates, loan amounts, and repayment periods can vary significantly between lenders, so it is essential to shop around and choose the loan that best suits individual needs and financial circumstances. Online loan comparison tools can be helpful in this process, allowing homeowners to easily compare multiple loan offers side by side.

In conclusion, financing wood countertops using personal loans offers several advantages for homeowners. The flexibility, speed, and convenience of the application process, along with potentially lower interest rates, make personal loans an attractive option for those looking to upgrade their kitchen or bathroom. However, homeowners should carefully consider their financial situation and repayment capabilities before committing to a personal loan. By doing so, they can enjoy the beauty and functionality of wood countertops while maintaining their financial stability.

in Charleston, SC

in Charleston, SC